This week I am due to be in Dubai presenting courses on Procurement and Supply Chain Management. Instead I am at home writing material for the Chartered Institute of Procurement & Supply, which in some ways suits as it is nice to have a few days in a row to write rather than clutching hours here and there.

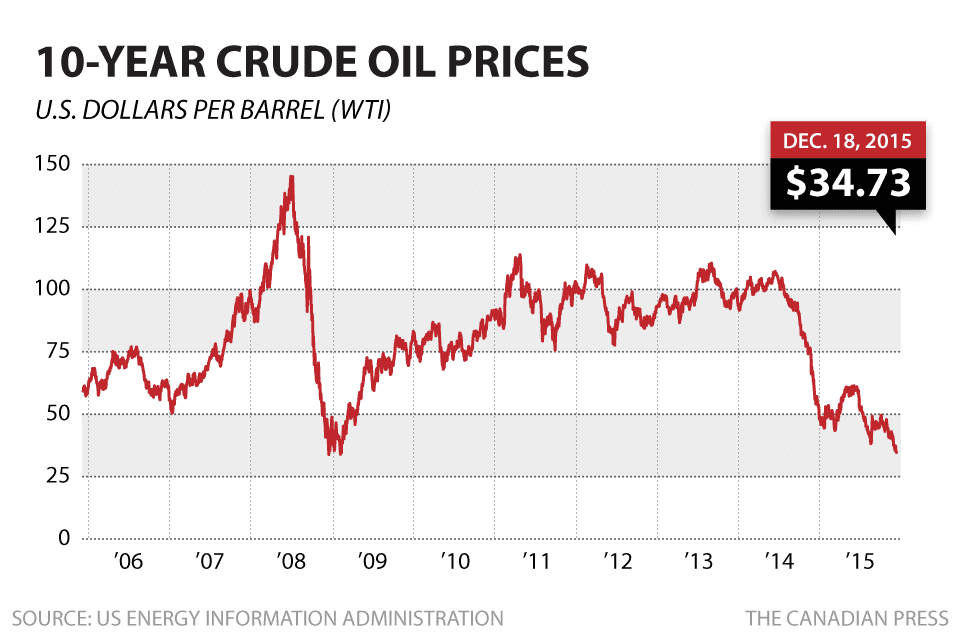

So far this year we have cancelled 5 weeks worth of courses in or for the Middle east, which is not surprisingly dominated by the oil and gas industry. The dramatic fall in the price of oil (currently about $41/barrel down from over $100) has meant a massive cut in spending on training across the ME and in particular the oil and gas sector.

Now I have a vested interest in this because I work as a trainer, but I think we should make the case that training in procurement and supply (above other things) should be protected because it

should pay for itself.

The usual argument is that when there is a financial shock it is sensible to cut back on discretionary spend - don't spend money unless you have to. And I don't argue with that.

However Procurement in the oil and gas industries in recent years has been focussed on Quality, delivery, availability, effectiveness and other non-price issues. The high price of oil, and the relatively high margins it gave, meant that Price was not the dominant issue. Now we are in a different environment.

Now Safety and Quality are things that cannot be comprised in process industries, but we can pivot to put far greater emphasis on price and cost rather than issues such as flexibility or efficiency. That does require a change within the organisation, and a change in emphasis for the Procurement team and Suppliers.

In some situations that may mean a focus on partnership and joint cost reduction. In others it may moving to a much more adversarial relationship than before. The trick is in deciding where and when.

Which is where training comes in. Training is not just about learning new things. It is also where we can go back to basics and build up again in a new pattern. It is where we can challenge established ideas and established ways of thinking. It is where we can learn from others and test new concepts in a risk free (or low risk) environment. In good training it is where we can plan how we are going to deliver in this new world.

In short a Procurement and Supply Chain training course could, and perhaps should, allow delegates to come away to save ten or more times the cost of the training. At the least delegates should come away with some plans to save the cost of the event within a tight timescale (perhaps 3 months). Those savings will then repeat over coming months adding multiples to the overall cost reduction.

The Return on Investment on Procurement training is high anyway, but when you need to save a lot of money in a hurry it is even better. Particularly if it allows you to avoid making "savings" that will in the end cost more through lost production.

OK, you can say that I am self-serving in making this argument, but I think it makes sense. In a losing football team you need to stop conceding goals. You don't do that by getting rid of the Goalkeeper.